LTGG presents

VIRTUALLY

LIMITLESS

“There is no hope for television by means of cathode-ray tubes.”

John Logie Baird

Your capital is at risk. Past performance is not a guide to future returns. The data in this series is based on a representative portfolio. As such, stock examples may not be held in every client portfolio, and performance, holding dates and returns may differ.

A history of opportunity

In 1926, John Logie Baird gave the first public demonstration of a working television.

He continued to tweak and perfect his creation over the ensuing couple of decades, right up to his death in 1946. What followed was one of the fastest consumer adoption stories of the modern era. Television ownership in the US rose from just 9 percent of households in 1950 to approximately 90 percent by 1960. ‘Prime time’ TV saw huge captive audiences, monetised by the dominant broadcasters of the day.

Over the next four decades, the household entertainment landscape enjoyed relatively stable economics and business models, but that didn’t preclude new business models from being built on top of the television set.

.webp)

By the 1980s, gaming was evolving from a niche pastime into a mass-market form of entertainment, led by the likes of Sega and Nintendo whose consoles plugged into TV sets.

Home video recorders then brought film into the living room on the consumer’s terms: first through VHS, which underpinned Blockbuster’s video rental model, and later through DVDs, which made distribution easier still and catalysed Netflix’s DVD-by-mail service. Each of these innovations gave consumers a little more control and gradually chipped away at the old broadcast model.

Over the lifetime of Long-Term Global Growth (LTGG), however, the pace of change has accelerated with a major shift from scheduled to on-demand consumption, enabled by the internet and turbocharged by the smartphone.

We have also seen a move from passive consumption to active participation. As leisure, entertainment and conversation moved online, user needs increasingly revolved not just around content, but also identity, community and belonging. Social media platforms and user-generated ecosystems emerged to meet this demand, harnessing participation to create a powerful network effect.

The ways we've unlocked the opportunity

In LTGG, we are always looking to anticipate where long-term value will accrue and where it may evaporate.

This consideration is especially relevant in the entertainment industry, where early growth can be spectacular. However, enduring winners are shaped by deeper forces: who owns the user relationship, who controls discovery and who can translate engagement into durably high returns.

In early 2007, when LTGG was approaching its third birthday, Steve Jobs launched the iPhone, to the derision of many industry analysts and competitors.

But over the ensuing decade, the iPhone drove an S-curve of smartphone adoption, which closely mirrored that of John Logie Baird’s brainchild almost five decades earlier.

This was a transition that opened a world in which content was no longer tied to a time, place or broadcaster. The old ‘golden age’ of captive audiences began to fragment.

The diverging fortunes of Netflix and Blockbuster were emblematic of this shift. The former understood early that viewing would move toward streaming, convenience and consumer control. The latter remained in denial and tied to the old model.

For us, the motivations and aspirations of management matter enormously.

Early in our interactions with Netflix co-founder Reed Hastings, we recognised both long-term vision and a rare willingness to adapt.

By the time we bought Netflix for the LTGG portfolio in 2015, the company had successfully pivoted from DVD rental to streaming. And the ecosystem would continue to broaden from there into original content, advertising and gaming.

“…this is about a ‘50-year franchise’ and to invest in Netflix one needs to share both his on-demand vision and trust their ability to execute on this opportunity.”

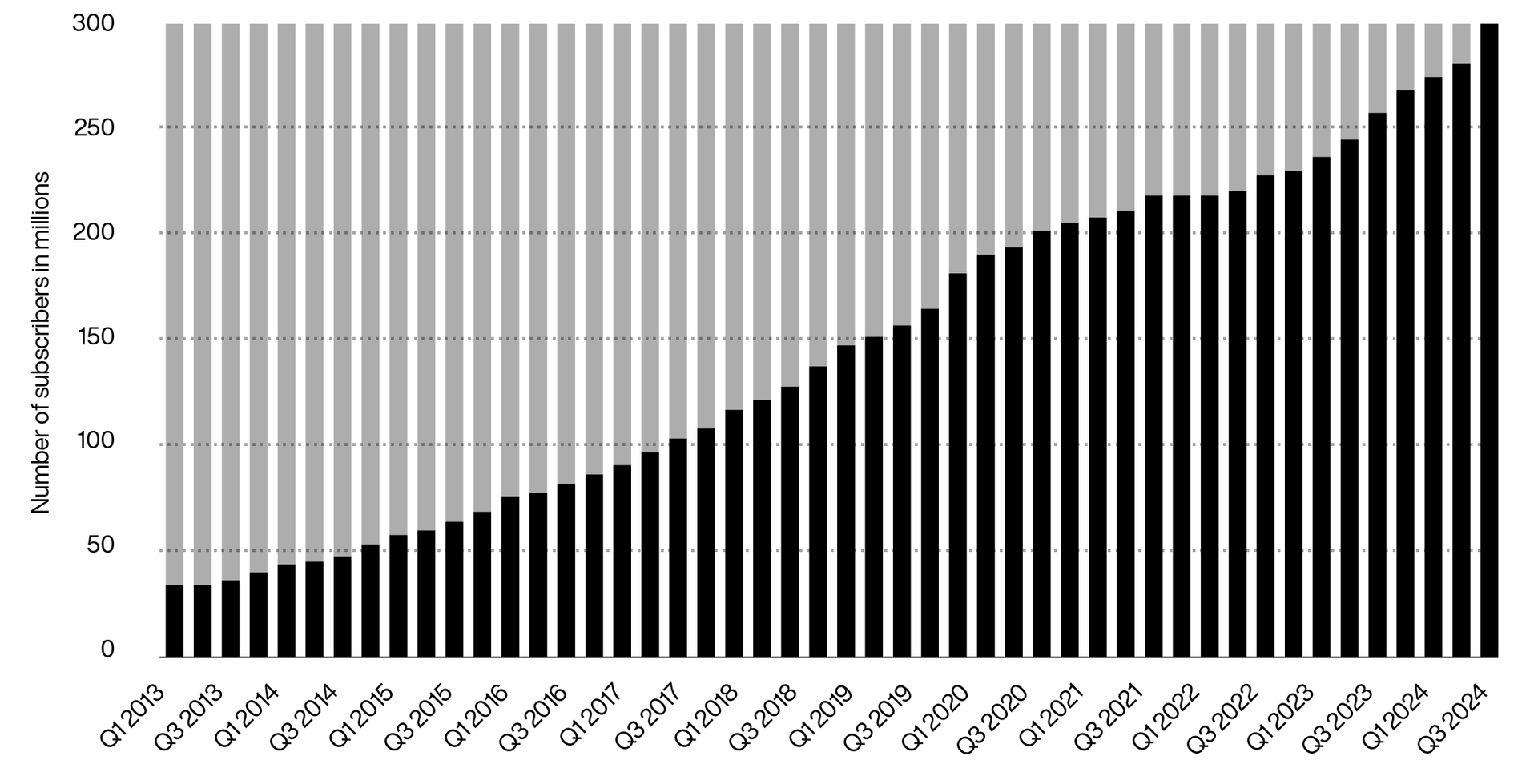

Number of Netflix paid subscriptions

From 1st quarter 2013 to 4th quarter 2024 (in millions)

Over the decade that followed our purchase, Netflix grew its subscriber base about fivefold to more than 300 million. That scale, allied with tremendous pricing power, transformed the economics of the business, driving sharp improvements in margins and returns during our ownership. The more important question now is whether the direction of returns from here remains as favourable, or whether much of that economic transformation is already behind it.

Spotify has a similarly imaginative founder. Long before the company’s public listing, we had come to know founder Daniel Ek well.

His vision was to build a place of discovery rather than simply a music streaming tool. By broadening the platform to include podcasts, audiobooks and personalised content, Spotify has deepened engagement, grown paid subscribers more than seventeenfold and expanded revenues eightfold since it was purchased for the portfolio in 2018. The company’s outlier potential from here now depends on a period of harvesting, with margins improving through a better revenue mix, stronger advertising economics and a leaner cost base.

In gaming, the greater prize often lies not in launching the hit title, but in owning distribution, identity and the player relationship around it. One of our research notes captured this neatly in relation to another LTGG holding, Tencent:

“[It] doesn’t even need to be any good at making games to be successful, such is the strength of its wider ecosystem.”

Tencent was built for the mobile era. By integrating gaming into social apps with more than two billion monthly active users, Tencent built an unrivalled route to reaching potential players and became the largest online gaming company in the world.

That ecosystem strength has continued to drive engagement, growth and strong returns since our initial purchase in 2009. Today, Tencent acts as a central nervous system for China's digital economy, with hundreds of billions of dollars in direct revenue and trillions of dollars in third-party economic activity flowing through its ecosystem.

Our later investment in SEA in 2022 reflected a Southeast Asian variant of the same insight. Garena, SEA’s digital gaming platform, serves as the entry point into a wider ecosystem spanning ecommerce and payments.

Not all our investments in this area have been successful. Our early enthusiasm for Nintendo was based on the company’s pioneering approach to social gaming in the living room with the Wii, a home video-game console that prioritised innovative, physically active gameplay over high-end graphics. But Nintendo then struggled to adapt to a mobile-first world and remained exposed to hardware cycles. NetEase, meanwhile, showed that strong content franchises and development capabilities alone are insufficient when distribution power and ecosystem control shift elsewhere, and much of its lunch was eaten by Tencent.

From content to community

As leisure, entertainment and conversation moved increasingly online, the most powerful platforms were not simply those with content, but those built around identity, contribution, trust and network effects. Our early work on Facebook (now Meta) captured this well.

“The network is based on real identities – this real identity sounds simple, but I think it is crucial in understanding Facebook’s success compared to previous iterations of social networks as it places real friends at the centre of the experience.”

What distinguished Facebook was not just scale, but the fact that it became embedded in users’ daily lives.

Facebook pulled people back constantly because it was built around real relationships, identity and habitual engagement. And over time, Meta translated that engagement into one of the most effective advertising machines in history. We decided to sell the stock in 2022 after a fourfold return over a decade because we struggled to pin down how it could grow to multiples of its $320bn market capitalisation at the time. But in hindsight, this was too early as we underestimated Meta’s adaptability and opportunity set in a world of distributed artificial intelligence.

LinkedIn reflected a similar insight in a different context. One of our early research notes observed that “It is evolving into a standard product and an online identity for professionals… the needs it addresses become continuous.” Here too, the same combination of digital identity and repeated engagement unlocked client returns until Microsoft’s takeover in 2016.

But not all our investments have successfully unlocked the economics of network effects.

Our investment in Peloton was founded on the premise that it could successfully grow and monetise a two-sided connected fitness network of instructors and erstwhile gym members.

But weak execution following a surge in pandemic-related demand meant the company failed to deepen engagement in the most valuable part of its ecosystem, and we moved on from the holding in relatively short order. In the world of travel, Tripadvisor built a valuable audience by harnessing user reviews and reducing uncertainty in travel decisions. The reviews and community were real assets, but much of the engagement sat in the planning phase, which meant that too much of the value was ultimately captured elsewhere in the journey.

More recently, Roblox and Reddit have offered two distinct yet compelling participatory platforms.

Roblox has inverted the traditional gaming model by building a user-generated ecosystem in which a large proportion of its users are creators as well as consumers. That makes it feel less like a game publisher and more like a place where users socialise, build identity and spend money on self-expression and virtual goods.

Retailers continue to experiment with different formats on the Roblox platform. By way of example, IKEA’s recent Roblox offering allows players to run their own virtual IKEA store and interact with products in a social, role-play environment, setting a new standard for experiential retail. The power here lies not just in gameplay, but in community and participation that can be monetised.

Reddit, by contrast, is built around more than 100,000 online communities. The users – more than a billion of them – do not simply scroll; they arrive with questions on all manner of topics, from how to fix a leaking dishwasher to how to navigate a divorce.

This corpus of accumulated real-world relevance leaves Reddit uniquely positioned in a world of ‘AI slop’. We’re attracted to the deeply engaged yet still under-monetised user base and a large gap between the strength of the product and the maturity of the business. As monetisation tools improve, that gap has meaningful room to close.

Opportunities looking forward

The next phase of this transformation is unlikely to be defined solely by content creation or distribution.

As artificial intelligence continues to accelerate and reshape the landscape further, the most important question is where the value accrues as digital experiences become more immersive and hyper-personalised.

With digital products becoming more effective at capturing attention, perhaps the scarcity will shift from content to trust, identity and genuine connection.

In the LTGG Team, our task is to look beyond today’s winners.

Exploring different questions

We continue to explore questions that receive less attention than they should from most market participants:

Which communities are strong enough to support monetisation without weakening trust, utility or authenticity?

How will AI reshape creation, discovery, immersion and engagement across gaming, streaming and social platforms?

Which companies are building ecosystems that users increasingly spend their time in rather than visit fleetingly?

How will societal habits, norms and boundaries evolve as the world continues to digitise?

How will the emerging spheres of virtual and augmented reality affect smartphone-based business models?

Can streaming platforms remain as capital-light in the future as they have in the past?

Disclaimers

Annual performance to 31 March each year (net %)

| Investment type | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|

| Baillie Gifford Long Term Global Growth Investment Fund B-ACC | -10.3 | -16.7 | 26.9 | 5.9 | -2.3 |

| MSCI ACWI Index* | 12.8 | -0.9 | 21.1 | 5.3 | 18.0 |

| IA Global Sector | 8.4 | -2.7 | 16.7 | -0.3 | 13.4 |

Past performance is not a guide to future returns

The Long Term Global Growth Investment Fund aims to outperform (after deduction of costs) the MSCI ACWI Index, as stated in sterling, over rolling five-year periods. Prior to 1st July 2023, to outperform (after deduction of costs) the FTSE All-World index, as stated in Sterling, over rolling five-year periods. The manager believes this is an appropriate target given the investment policy of the Fund and the approach taken by the manager when investing. In addition, the manager believes an appropriate performance comparison for this Fund is the Investment Association Global Sector.

There is no guarantee that this objective will be achieved over any time period and actual investment returns may differ from this objective, particularly over shorter time periods.

Important Information

This communication was produced and approved in May 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

This communication does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co Limited is authorised and regulated by the Financial Conduct Authority. Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

A Key Information Document is available at bailliegifford.com.

Investment markets can go down as well as up and market conditions can change rapidly. The value of an investment in the Fund, and any income from it, can fall as well as rise and investors may not get back the amount invested.

The specific risks associated with the Fund include:

- Custody of assets, particularly in emerging markets, involves a risk of loss if a custodian becomes insolvent or breaches duties of care.

- The Fund invests in emerging markets, which includes China, where difficulties with market volatility, political and economic instability including the risk of market shutdown, trading, liquidity, settlement, corporate governance, regulation, legislation and taxation could arise, resulting in a negative impact on the value of your investment.

- The Fund's concentrated portfolio relative to similar funds may result in large movements in the share price in the short term.

- The Fund has exposure to foreign currencies and changes in the rates of exchange will cause the value of any investment, and income from it, to fall as well as rise and you may not get back the amount invested.

- The Fund's share price can be volatile due to movements in the prices of the underlying holdings and the basis on which the Fund is priced.

Further details of the risks associated with investing in the Fund can be found in the Key Investor Information Document or the Prospectus, copies of which are available at bailliegifford.com.