LTGG presents

BREAKING

BANKS

“Bank credit is the pavement along which production travels; and the bankers, if they knew their duty, would provide the transport facilities…”

John Maynard Keynes, A Treatise on Money, 1930

Your capital is at risk. Past performance is not a guide to future returns. The data in this series is based on a representative portfolio. As such, stock examples may not be held in every client portfolio, and performance, holding dates and returns may differ.

A history of opportunity

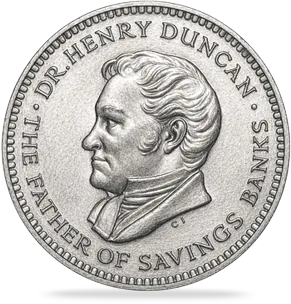

The world’s first savings bank is just a couple of hours’ drive from Baillie Gifford’s headquarters. In 1810, the minister Henry Duncan invited his parishioners in Ruthwell, south-west Scotland, to bring in a few shillings at a time.

He updated the ledgers by hand, issued passbooks and lent the money cautiously within the parish. The promise was simple: safety, thrift and a modest return.

Two-and-a-bit centuries on, most of us still ask our banks for much the same service. We pay in our salaries, make payments and occasionally borrow. The passbook has become an ‘app’, and the minister has been replaced by a branch, a call centre or a chatbot, but a Ruthwell parishioner would recognise the basic bargain.

While transport has moved from horses to electric vehicles, and communication has leapt from letters to video calls, banking, by comparison, ambled along the same country road.

For much of the twentieth century, banks provided “good enough” utility. Innovation focused on channels – cheques, ATMs, phone banking, online, then mobile – rather than on reimagining the underlying relationship or economics.

Fees and spreads were often high and opaque, and the perceived hassle of moving one’s financial life created inertia. Regulation, for understandable reasons, acted as a moat.

While banks have been in no hurry to evolve, the world around them has been sprinting – nowhere more so than in Asia.

In the space of two decades, Asia’s GDP has compounded at twice the pace of the developed world and now accounts for nearly half of the global total.

The consumption that has driven this growth has been enabled by hundreds of millions of people in the region opening their first formal payments or savings accounts over the same period.

The ways we’ve unlocked the opportunity

From the perspective of a long-term growth investor, traditional banks have often appeared heavily regulated and structurally constrained. That sits awkwardly with LTGG’s philosophy: a stock-driven, patient strategy looking for a small number of companies that can become multiples of their current size over the next 10 years and beyond. Where we have invested in finance providers, it has been because we have had conviction in management’s ability to deploy capital, or because a company has been early in addressing a dynamic and growing opportunity.

Our long-time holding in the Indian company, HDFC Corporation, rested on this combination: a pure-play mortgage lender riding a long runway of rising mortgage penetration (which was just 7 per cent of GDP when we invested in 2004, and has roughly doubled since), run by an unusually disciplined and thoughtful management team. Deepak Parekh and Keki Mistry embedded a culture of “profitability over market share” and a pragmatic willingness to slow growth or pull back from riskier segments when conditions warranted. LTGG held the shares for two decades and generated a near tenfold return, choosing to sell when these advantages were diluted amid corporate activity as HDFC Corporation and HDFC Bank merged.

Our investment case in the late 2000s for current holding, Tencent, embraced the optionality offered by its payment services as part of its wider gaming, social and ecommerce ecosystem.

In the years since, Tencent's WeChat Pay has leapfrogged traditional banking services for many in China, becoming part of citizens’ everyday lives. WeChat Pay accounts for 40 per cent of China’s mobile payment market and is used for peer-to-peer transfers, taxis, shopping and utility bills. For many users there is no conscious decision to “go to the bank”. Payments and small loans simply appear as options inside their chat feed – a stark contrast with the static passbook at Ruthwell.

"We know that their data sets and skills overwhelm any other Chinese players [incumbent banks]….the likelihood of leadership, success and returns seem to me to be high – I’d much rather take the bet that there are substantial earnings here in 10 years than in banks (local or Western)."

A couple of other holdings were less successful. The fault lines in the investment cases of Banco Santander, the Spanish small-business lender, and Lending Club, the marketplace lending platform, were distinct. In the former’s case, a marked shift in the post-financial crisis regulatory environment curtailed the likelihood of sufficient returns, while in the latter’s case, governance failures and managerial change derailed our long-term investment case.

After decades of barely visible evolution, banking looks poised for its own Cambrian burst. The possibility of transformational growth in financial services is emerging, not within the traditional branch network, but in the software and platforms being built around it.

As financial activity migrates from balance sheets and bricks to code and data, the unit economics of the old model look increasingly outdated. In many of the most interesting cases, this shift is being driven by founder-led cultures with deep technical expertise and long-term ambitions.

Managing complexity and security: payments infrastructure

If Ruthwell’s ledgers were the local roads of the banking system, today’s global payment networks are its railways and flight paths.

An LTGG research note from a few years ago observed that “companies that help merchants manage complexity in payments will grow in importance and value in the coming years. Adyen is one such company. It stands out from others.” Adyen provides a single, global software platform that replaces the patchwork of acquirers, gateways and processors many merchants have historically stitched together.

Our strengthened conviction in the investment case is based on how this Dutch payments business addresses the underlying challenges. Founder Pieter van der Does and his team see payments not as a financial problem to be solved by banks, but as an engineering problem to be solved with software. Engineers are the largest staff cohort. When Adyen stepped up hiring of engineers, near-term margins fell, and the share price suffered. Management’s response was unapologetic: the company is built for long-term growth, and people are its main use of capital. Our question was whether this investment was translating into a durable advantage. The evidence so far is encouraging.

Revenue growth has been consistently strong (more than 20 per cent per annum), customer churn has been very low (less than 1 per cent), and much of Adyen’s growth has come from existing merchants expanding across regions, channels and products.

This supports our view that Adyen is differentiated and delivering utility to its customers. One example is its Uplift product, which leverages its platform-level data to route transactions most efficiently, lowering costs by up to a quarter and increasing authorisation rates.

Against a global payments pool measured in the tens of trillions of dollars, Adyen’s annual payment volumes (more than $1tn) still feel modest. The market is many multiples larger, and with 40 per cent of global payment volumes still in cash, we think the odds of extreme positive outcomes increase as scale grows.

Removing friction: neobanking

There has also been a rebirth of the bank itself, in digital form. Neobanks promise familiar things – a safe place to store money, ways to pay, access to credit – but with radically different cost structures and cultures.

Nubank’s branchless, fully digital model means it can serve customers that incumbents find unprofitable. CEO David Vélez has been instrumental in driving the scalability of the business, seeking to build a platform that will enable the company to launch in a new country “with no more than 12 staff and less than a $1m outlay”.

Incumbent banks in Nubank's markets are burdened with sprawling branch footprints and high fixed costs

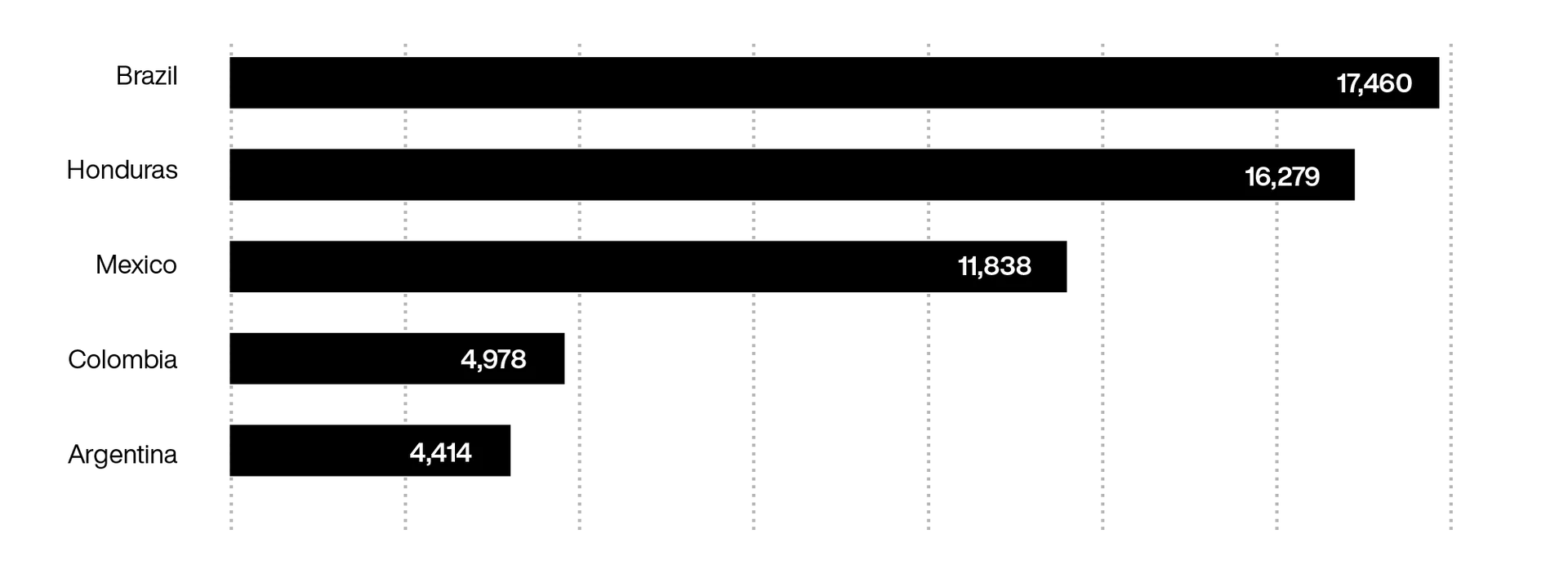

Nubank has over 100 million customers reaching more than half of Brazil’s adult population, and early evidence suggests its product-market fit in Mexico and Colombia is, if anything, stronger. In Mexico, Nubank's net promoter score, which is in the mid 90s, is described as “the highest of any consumer company in the world.”

We are under no illusion: Nubank remains a bank, exposed to credit cycles, regulation and competition. But it is also something genuinely new – a branchless, software-native institution that has signed up tens of millions of customers and set a new bar for what a bank can feel like in Latin America. It combines Ruthwell’s essential function with radically different economics and a culture of fast, iterative development. This mix gives us credible routes to the kind of multi-fold growth outcomes we are looking for in LTGG.

Integration with commerce: embedded finance ecosystems

Perhaps the most interesting developments lie in companies where finance is not the main story at all. It is woven into activities like shopping, messaging and running a business, strengthening existing moats built on engagement, data and network effects.

SEA is building just that across south-east Asia. Shopee, its ecommerce platform, is a leading shopping app in the region, while its gaming arm, Garena, remains a powerful cash engine. Monee, its financial arm, offers wallets, payments and credit in markets where large parts of the population remain underbanked.

Finance here is not an isolated vertical; it is a way to deepen engagement and monetise an existing audience. What is most exciting is that CEO Forrest Li, argues that finance may ultimately prove a larger opportunity than retail itself because “retail is only a part of the consumer wallet, whereas financial services are the whole wallet”.

Another of our holdings, MercadoLibre (MELI), purchased in late 2022, shows how culture and local knowledge can turn potential into reality in Latin America. MELI began as a marketplace in Argentina and is now the leading ecommerce and fintech platform across the region. Its expansion has been no spreadsheet exercise.

Our research noted that founder Marcos Galperin and his colleagues displayed “candour, ambition and a clear understanding of where they are heading”. They have shown a repeated willingness to sacrifice near-term margins – whether by over-investing in logistics, increasing R&D spend or proactively slowing credit originations in riskier segments – to protect long-run advantage in markets “where cycles can be fatal”.

Over 40 per cent of MELI’s revenues now come from financial services, in a region where many people still have limited access to formal banking and cash remains important. Credit operations have grown quickly but are deliberately conservative in ticket size and duration. That mix of local realism and long-termism is, in our view, what has unlocked MELI’s growth so far.

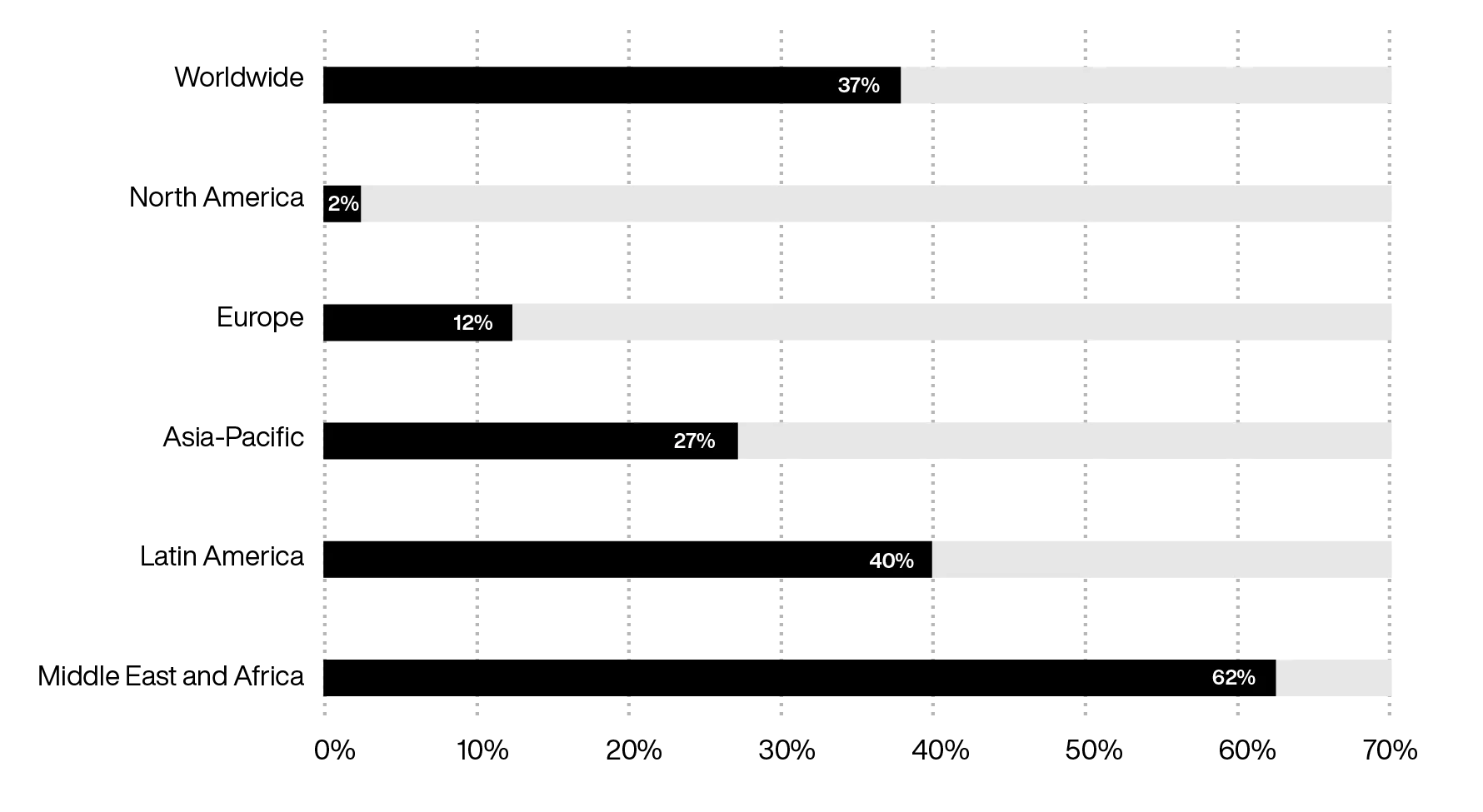

Latin America has the world’s second-highest proportion of unbanked adults

The opportunities looking forward

If Henry Duncan and his parishioners were to recognise the banking proposition today, they would have to look harder in the years ahead.

As financial services are rebuilt on software rails and embedded into powerful ecosystems, value capture becomes more fluid, accruing across a wider range of players in an ever-expanding financial ecosystem.

The greatest risk, in our view, is to ignore the structural changes underway and thus miss the compounding that can come from being roughly right about the small number of companies helping to write that next chapter of financial life.

For LTGG, this is both a challenge and an opportunity.

Exploring different questions

We continue to explore questions that receive less attention than they should from most market participants:

Where will “the bank” actually live – as a standalone institution, or inside the software, platforms and devices people already use?

Who will control the critical rails and data, and how might that shape the return landscape over decades rather than quarters?

What happens when the marginal cost of basic banking approaches zero – where does profitable differentiation then come from?

How far can embedded finance go before regulators redraw the map of responsibility and risk, and which parts of the value chain – insurance, pensions, SME finance, treasury – are still waiting to be rebuilt?

Disclaimers

Annual performance to 31 March each year (net %)

| Investment type | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|

| Baillie Gifford Long Term Global Growth Investment Fund B-ACC | -10.3 | -16.7 | 26.9 | 5.9 | -2.3 |

| MSCI ACWI Index* | 12.8 | -0.9 | 21.1 | 5.3 | 18.0 |

| IA Global Sector | 8.4 | -2.7 | 16.7 | -0.3 | 13.4 |

Past performance is not a guide to future returns

The Long Term Global Growth Investment Fund aims to outperform (after deduction of costs) the MSCI ACWI Index, as stated in sterling, over rolling five-year periods. Prior to 1st July 2023, to outperform (after deduction of costs) the FTSE All-World index, as stated in Sterling, over rolling five-year periods. The manager believes this is an appropriate target given the investment policy of the Fund and the approach taken by the manager when investing. In addition, the manager believes an appropriate performance comparison for this Fund is the Investment Association Global Sector.

There is no guarantee that this objective will be achieved over any time period and actual investment returns may differ from this objective, particularly over shorter time periods.

Important Information

This communication was produced and approved in May 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

This communication does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co Limited is authorised and regulated by the Financial Conduct Authority. Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

A Key Information Document is available at bailliegifford.com.

Investment markets can go down as well as up and market conditions can change rapidly. The value of an investment in the Fund, and any income from it, can fall as well as rise and investors may not get back the amount invested.

The specific risks associated with the Fund include:

- Custody of assets, particularly in emerging markets, involves a risk of loss if a custodian becomes insolvent or breaches duties of care.

- The Fund invests in emerging markets, which includes China, where difficulties with market volatility, political and economic instability including the risk of market shutdown, trading, liquidity, settlement, corporate governance, regulation, legislation and taxation could arise, resulting in a negative impact on the value of your investment.

- The Fund's concentrated portfolio relative to similar funds may result in large movements in the share price in the short term.

- The Fund has exposure to foreign currencies and changes in the rates of exchange will cause the value of any investment, and income from it, to fall as well as rise and you may not get back the amount invested.

- The Fund's share price can be volatile due to movements in the prices of the underlying holdings and the basis on which the Fund is priced.

Further details of the risks associated with investing in the Fund can be found in the Key Investor Information Document or the Prospectus, copies of which are available at bailliegifford.com.