LTGG presents

INFINITE

COMPUTE

“Any sufficiently advanced technology is indistinguishable from magic.”

Arthur C Clarke

Your capital is at risk. Past performance is not a guide to future returns. The data in this series is based on a representative portfolio. As such, stock examples may not be held in every client portfolio, and performance, holding dates and returns may differ.

A history of opportunity

“Machine intelligence is the last invention that humanity will ever need to make.” When that line was written by philosopher and futurist Nick Bostrom in his 2014 book Superintelligence: Paths, Dangers, Strategies, it read provocatively. In a decade from now, it could seem very prescient.

The launch of OpenAI’s ChatGPT in late 2022 involved machine intelligence becoming accessible, repeatable, and usable at a global scale. It was also a lightbulb moment in public consciousness, as it became the fastest consumer application to reach 100 million users.

The pace of improvement in artificial intelligence capabilities is now accelerating at breakneck speed.

Scale up, scale out and specialise

Early computers were room-sized machines powered by vacuum tubes and punch cards.

In 1956, at the Dartmouth Summer Research project, the term "artificial intelligence" was coined. But the compute to realise it did not exist: AI was an ambition without infrastructure.

It was the microprocessor revolution that set Moore’s Law into commercial motion. Catalysed by Intel’s 4004 microprocessor in 1971, an entire central processing unit (CPU) was compressed onto a single chip. This steady doubling of transistor density gave the industry a dependable roadmap. Computing became cheaper, faster, and smaller. Baillie Gifford’s first PC was the size of a modern-day fridge, but by 1993, we’d rolled out far more manageably-sized Dell Optiplex computers.

By the late 1990s, over half of US households owned a PC and office floors were transformed. Computers were no longer the sole domain of IT departments.

The growing network of distributed systems laid the architectural foundations of cloud computing, separating compute from ownership and lowering barriers to software adoption. This spawned search engines, social networks, and ecommerce platforms and facilitated the explosion of mobile devices.

By 2015 there were more mobile phone contracts than people on Earth. This ecosystem generated data at a previously unimaginable scale.

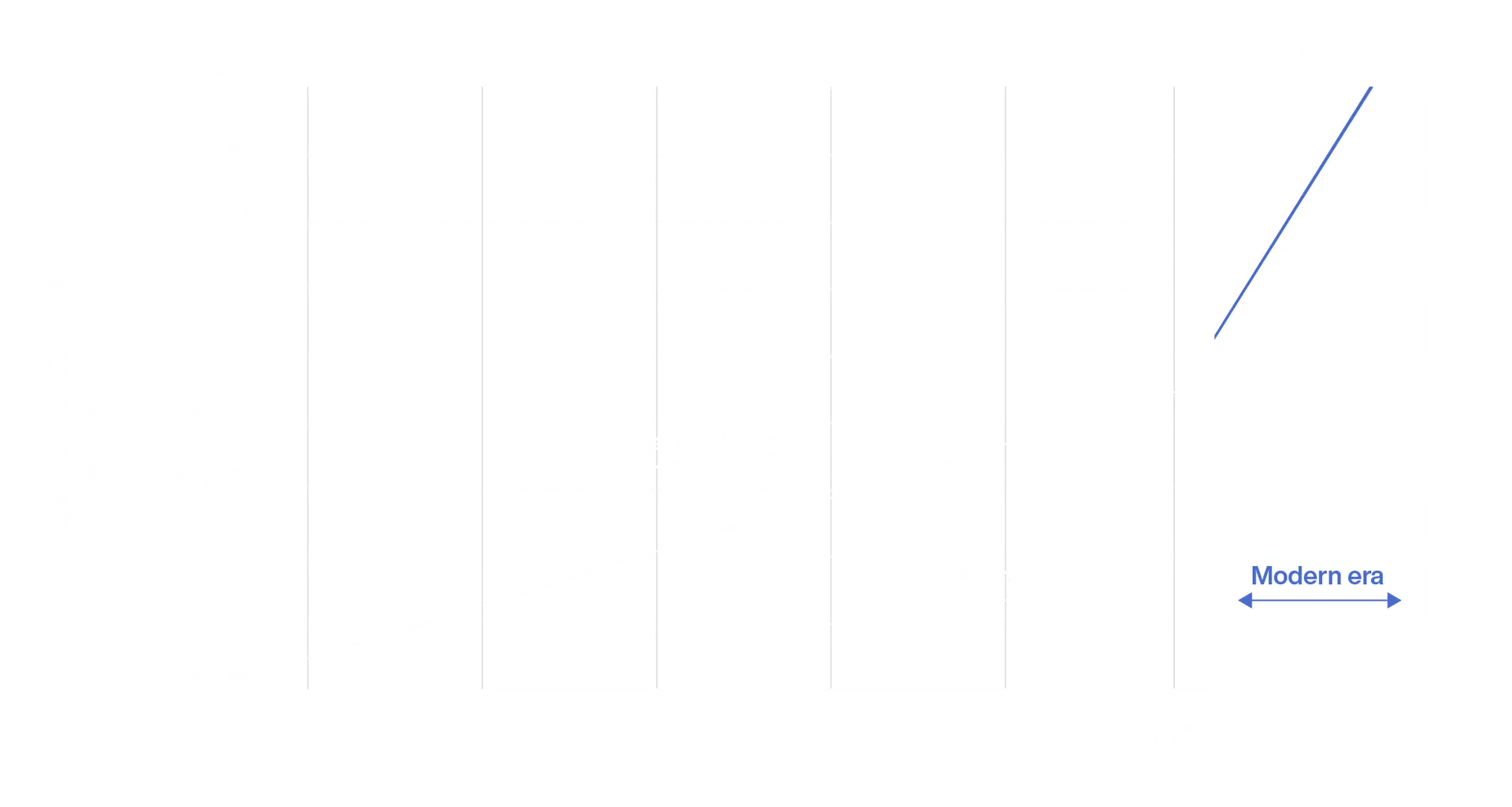

In the early 2010s, computing hit an inflection point. Machine learning began compounding at a pace that made Moore’s Law look pedestrian. The Graphics processing units (GPUs) that had been designed to paint pixels for video games, proved perfect for the parallel number crunching of large datasets. The milestones that followed were proof of a new production function.

Training compute of milestone machine learning systems over time

Much of this progress has unfolded during LTGG’s lifespan.

For two decades, accelerating compute has been the force behind many of our best growth opportunities, first in hardware, then in cloud infrastructure, and now in AI-native applications.

The ways we’ve unlocked the opportunity

LTGG has always engaged early with those laying the foundations of structural change.

That means eschewing conversations about next quarter's earnings and probing deeper. When we first invested in Amazon in 2004, our investment case centred on ecommerce growth. But in early conversations with Jeff Bezos, it became clear that he was thinking beyond product lines or geographies. He focused instead on falling input costs (CPU power, bandwidth and storage), which were getting “twice as cheap every 12–18 months.” His question was not how many books could be sold, but: “What can you do with 30 times as much disk space, 20 times as much computing power and 30 times as much bandwidth?”

When Amazon launched Amazon Web Services (AWS) in 2006, investment markets barely noticed. But what looked like a side project would become one of the most profitable infrastructure businesses in modern history.

AWS has grown its revenues 40-fold since 2013, accounts for 60 per cent of Amazon’s profits today and offers over 200 services to customers. This dynamic has played a significant part in driving the more than 100-fold return for LTGG clients over our holding period, with AWS continuing to compound impressively at scale.

More widely, our research has recognised the industrialisation of access to compute and acknowledged this as a “30-40-year opportunity”. This consideration led us to invest in the likes of Alphabet and Chinese company Tencent, whose leading search and social media services were similarly compute-intensive and spawned cloud computing platforms of their own.

“We’ve discussed the importance of scale in software businesses in the past, but it seems increasingly apparent that the long-term spoils will accrue, disproportionately, to the very largest.”

A cambrian opportunity

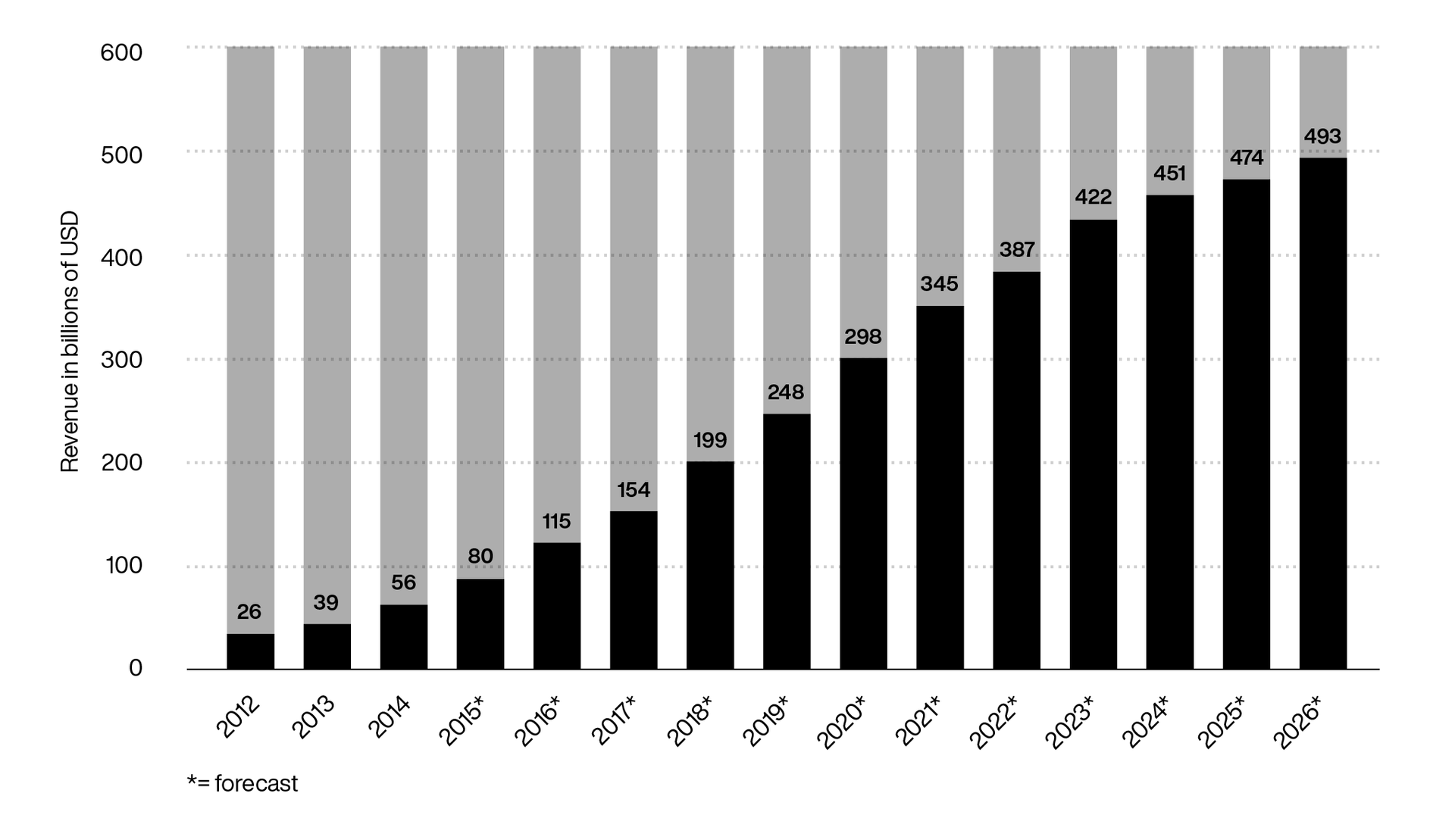

Whilst LTGG benefitted handsomely from the already huge companies becoming even larger, the collapsing marginal cost of cloud software also sparked a Cambrian explosion of new business models and associated investment opportunities: one was cloud-based enterprise software.

Revenues of public cloud service providers worldwide from 2012 to 2026

LTGG’s approach was, as always, highly selective, seeking to invest where scale was being built, innovation was accelerating and returns were high or strengthening.

We invested in Salesforce at a time when the market’s appreciation of scale was still largely confined to margin potential rather than growth durability. Our focus was different. We were interested in what scale did to time.

It shortened upgrade cycles, tightened feedback loops between usage and product development, and strengthened renewal dynamics. Salesforce compounded revenues in the high twenties for over a decade, scaling from $1.7bn to over $30bn before we exited in 2023, delivering a return in excess of 5x for LTGG clients.

Elsewhere, we saw similar potential in Workday; a chance to leverage leadership in human capital management (HCM) software into a broader system of record for the enterprise, particularly finance. Over our decade-long holding period, revenues grew more than fifteenfold, but the investment return was good rather than stellar. The path beyond HCM proved more incremental, and sustained marketing spend curtailed long-term profit growth.

Sometimes our investment theses on earlier-stage companies explicitly acknowledged that competitive positions were still being formed, but the upside skew looked attractive. On LTGG, we often talk of holding contentions passionately but lightly, and inevitably, some of the competitive dynamics played out less favourably than expected.

Rackspace was a case in point: an early leader in cloud hosting, it was rapidly commoditised as hyper-scalers such as AWS and Microsoft Azure captured the economics through superior scale and breadth. Splunk, meanwhile, tackled a real need in unstructured data management, but execution slipped; positioning became muddled, and leadership churn sapped confidence. We exited after four years with a disappointing outcome.

Patterns have emerged as we have navigated these opportunities. Cloud winners are built on recurring relationships, data accumulation and rapid product iteration, allowing growth to endure far longer than traditional software cycles suggest.

Yet cloud architecture and scale are not sufficient on their own. The flywheel only spins with disciplined execution, clear product direction and a model that converts scale into stronger returns. Where those elements align, as with AWS, the outcomes can be transformational.

Value in bottlenecks

“The applications of deep learning are seemingly endless – autonomous driving, (near) instantaneous translation of spoken language, personal assistants, accurate image recognition, fraud detection, medical diagnosis…”

The LTGG investment process revolves around the unlocking of optimistic upside scenarios.

When we first invested in NVIDIA in 2016, its market capitalisation was around $35bn. The company was recognised as a strong graphics chip designer, but the scale of its future dominance in accelerated computing was far from consensus.

What became clear through engagement with leading AI companies was that GPUs were emerging as a critical bottleneck in model training and inference. And as demand increased, NVIDIA’s position strengthened.

Over the following decade, earnings grew at extraordinary rates, and the company became the near-monopolistic provider of frontier GPUs, delivering a 128-fold return for LTGG clients.

We extend that logic further down the stack. If GPUs were scarce, it was because the bottleneck had moved upstream into the tools and know-how required to keep shrinking transistors to one twenty-thousandth of the width of a human hair. Our work on ASML revealed why its position in extreme ultraviolet lithography machines (used to pattern the features that are later etched into wafers) is so defensible. It has been built over decades of iteration across thousands of precision parts and atop an installed base that generates hard-to-replicate services revenue.

That same lens also shaped our more recent purchase of TSMC, which commands over 70 per cent of the global semiconductor manufacturing market share. Its moat lies in its years of established practice, tight co-development with customers and process expertise that deepens with each generation, making the “leading edge” increasingly hard to catch.

The pursuit of infinite compute may feel expansive, but its progress depends on a surprisingly narrow set of enabling technologies. Recognising where those constraints lie remains central to how we seek to unlock opportunity.

Escape velocity

What makes a good leader in an era of accelerating compute? Our research has led us to several technical founders – not career CEOs – who are leading a charge that is changing the way we measure effectiveness and return on compute. They are not simply adopting AI as a feature; they are translating it into real-world outcomes that customers can measure and pay for.

The return on compute is increasingly expressed in terms of energy saved, miles driven more safely, factories run with less downtime, crimes solved faster, or campaigns converted more efficiently. For example, Samsara turns fleets and industrial equipment into measurable systems by tagging equipment with sensors and pairing them with AI. The result? Customers reduce idling, fuel use, accidents and maintenance surprises. At American Airlines’ Dallas Fort Worth hub, Samsara’s technology has saved ground staff hours of frustration searching for ground support equipment and reduced morning flight delays by 15 per cent.

In public safety, Rick Smith, the founder of Axon, is building the digital backbone of modern policing. Axon’s products are used by over 17,000 law enforcement agencies, with its cloud-based evidence management platform providing storage and management of digital evidence – including body-worn camera footage, in-car video, and case documents – while AI tools enable automated redaction, transcription, and search capabilities. Police departments have reported saving hours per shift simply by using AI to draft reports from body-worn camera footage.

In digital advertising, AppLovin founder-CEO Adam Foroughi is obsessive about incremental improvements to the company’s predictive capabilities. Its AI engine processes over 2.5 million ad decision requests per second, driving a powerful flywheel: better advertising outcomes attract greater engagement from advertisers and developers, which in turn generates more data.

Sitting underneath much of this is a different kind of moat: the rails and rulebook of the AI economy. Cloudflare is increasingly becoming the layer where the internet’s traffic is policed and steered, handling 6 trillion requests a day, giving it a front-row seat on what’s real, what’s malicious and what’s machine-generated. Founders Matthew Prince and Michelle Zatlyn see Cloudflare playing a critical role in the governance of the AI economy. For example, their Crawl Control offering enables online publishers to prevent AI companies from crawling their sites for data – not just a matter of IP protection but also an issue of cost control.

The same mindset is changing the economics of space.

Founder Peter Beck has scaled Rocket Lab into a business built around repeatability and cadence, with its Electron rocket engineered for rapid turnaround and the company now delivering record annual launch volumes. The long-term prize lies in deploying and ultimately operating satellite constellations in low Earth orbit, where value accrues not to the hardware alone, but to the services and intelligence it enables.

The opportunities looking forward

Periods of profound technological change often prompt the same reaction in investment markets: a fixation on failure. Which incumbents will be disrupted? Whose margins will collapse? Where will value be destroyed?

But for us in LTGG, the more interesting question is not what breaks, but who succeeds?

As machine intelligence propagates through the real economy, value will not accrue evenly. It may concentrate on those who design the accelerators, those who orchestrate the data, or those who embed intelligence directly into products and processes. Early advantages may prove durable – or fleeting – as models improve for everyone.

At the same time, new constraints are emerging.

Compute power has advanced exponentially, but electricity, cooling and grid infrastructure are becoming binding. If power rather than silicon becomes the limiting factor, it may be inevitable that some of the leadership in this area moves from west to east.

Across two decades, LTGG has sought not simply to observe technological change, but to engage with those shaping it. From early conversations with cloud pioneers to today’s dialogue with frontier AI labs such as OpenAI and Anthropic, alongside founders and academic partners, we have worked to ground our optimism in understanding.

Our task remains to identify and own the companies translating technological inflexion into enduring advantage. Those adapting fastest, compounding feedback loops most effectively, and offering the potential for truly outlier growth.

“The future is already here – it’s just not evenly distributed.”

Exploring different questions

We continue to explore questions that receive less attention than they should from most market participants:

If energy, not silicon, becomes the dominant constraint in AI deployment, how will this affect the distribution of compute capability? Where in the world will the frontier reside? What will this mean for our investable opportunity set?

Will AI consolidate enterprise software into fewer platforms, or enable fragmentation through agents and orchestration layers?

How durable are today’s hardware bottlenecks in the AI stack?

Does distributed inference reshape the hierarchy between hyperscalers and edge networks?

Which companies redesign workflows around AI, rather than simply layering it on top?

Disclaimers

Annual performance to 31 March each year (net %)

| Investment type | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|

| Baillie Gifford Long Term Global Growth Investment Fund B-ACC | -10.3 | -16.7 | 26.9 | 5.9 | -2.3 |

| MSCI ACWI Index* | 12.8 | -0.9 | 21.1 | 5.3 | 18.0 |

| IA Global Sector | 8.4 | -2.7 | 16.7 | -0.3 | 13.4 |

Past performance is not a guide to future returns

The Long Term Global Growth Investment Fund aims to outperform (after deduction of costs) the MSCI ACWI Index, as stated in sterling, over rolling five-year periods. Prior to 1st July 2023, to outperform (after deduction of costs) the FTSE All-World index, as stated in Sterling, over rolling five-year periods. The manager believes this is an appropriate target given the investment policy of the Fund and the approach taken by the manager when investing. In addition, the manager believes an appropriate performance comparison for this Fund is the Investment Association Global Sector.

There is no guarantee that this objective will be achieved over any time period and actual investment returns may differ from this objective, particularly over shorter time periods.

Important Information

This communication was produced and approved in May 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

This communication does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co Limited is authorised and regulated by the Financial Conduct Authority. Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

A Key Information Document is available at bailliegifford.com.

Investment markets can go down as well as up and market conditions can change rapidly. The value of an investment in the Fund, and any income from it, can fall as well as rise and investors may not get back the amount invested.

The specific risks associated with the Fund include:

- Custody of assets, particularly in emerging markets, involves a risk of loss if a custodian becomes insolvent or breaches duties of care.

- The Fund invests in emerging markets, which includes China, where difficulties with market volatility, political and economic instability including the risk of market shutdown, trading, liquidity, settlement, corporate governance, regulation, legislation and taxation could arise, resulting in a negative impact on the value of your investment.

- The Fund's concentrated portfolio relative to similar funds may result in large movements in the share price in the short term.

- The Fund has exposure to foreign currencies and changes in the rates of exchange will cause the value of any investment, and income from it, to fall as well as rise and you may not get back the amount invested.

- The Fund's share price can be volatile due to movements in the prices of the underlying holdings and the basis on which the Fund is priced.

Further details of the risks associated with investing in the Fund can be found in the Key Investor Information Document or the Prospectus, copies of which are available at bailliegifford.com.