LTGG presents

ELECTRIFYING

PROGRESS

“We will make electricity so cheap that only the rich will burn candles.”

Thomas A. Edison, Menlo Park, 1879

Your capital is at risk. Past performance is not a guide to future returns. The data in this series is based on a representative portfolio. As such, stock examples may not be held in every client portfolio, and performance, holding dates and returns may differ.

A history of opportunity

As a firm, we have a long history of navigating deep transitions in the energy and mobility markets.

In the early 20th Century, our holdings in the rubber industry were predicated on soaring demand for tyres as the Model T Ford catalysed the exponential growth in automobiles. We also held American railroad companies, oil companies and utilities such as Calcutta Electric Supply.

Each of these transformations was accompanied by a dose of creative destruction. The Model T Ford slashed demand for horse saddles, feed, and wagons. Calcutta Electric's success decimated the market for hand-pulled fans and oil lamps. This heritage of threading the needle through periods of great change sets the backdrop to Long Term Global Growth (LTGG).

Two decades ago, a number of traditional oil and gas companies featured in the original LTGG portfolio, but with global fossil fuel output flatlining, these are long gone. Our focus has instead shifted to three major transformations reshaping energy and mobility.

Shift 1: from energy as a commodity to energy as a technology.

Over the past twenty years, we've navigated a profound shift from energy as a finite commodity to energy as a technology, one that improves and cheapens dramatically over time. When LTGG was founded, installing a gigawatt of solar took over a year; today it takes less than a day. As a result, solar capacity has risen a thousandfold.

Installed solar energy capacity

Cumulative installed solar capacity, measured in gigawatts (GW).

Battery technology has advanced at a similar pace. Lithium-ion costs have plunged and energy density has roughly doubled, enabling longer-range EVs and more compact consumer electronics. New chemistries such as lithium iron phosphate (LFP) and sodium-ion have boosted safety, lifespan and resilience to critical mineral constraints, while gigafactories have driven costs down over tenfold.

Shift 2: changing car ownership.

Global auto growth has been modest, but the anaemic overall growth masks a dramatic geographic shift. When LTGG began, China had a mid-single-digit share of global auto manufacturing; today it is nearly 40 per cent. A plethora of new domestic brands has emerged, making award-winning vehicles with specification and performance levels that have left Western auto companies scrambling to respond.

Shift 3: changing car propulsion.

The third shift concerns how cars are powered. Just under a decade into LTGG, one of our research notes ventured that "In a world dominated by EVs, 100 years of engine IP and development becomes, if not worthless, at least worth a lot less than it is today". But although that view appears increasingly correct, our twenty years of investing in energy and mobility stocks have reinforced the importance of stock picking. Thematic investing is dangerous at the best of times, and a hypothetical basket of solar or EV stocks would have been disastrous.

As LTGG portfolio manager Mark Urquhart reflected on the solar industry a decade ago:

"I can't remember in my near twenty years at Baillie Gifford looking at an industry which is so fast growing in volume terms but so muddied and complex at the company level.

Against a very positive volume background, the conundrum remains of why companies are failing to translate this growth into revenues and profits. I hope one of our disciplines in LTGG has been to not force companies into areas which might seem hot in terms of growth if they can't answer our ten questions."

The ways we've unlocked the opportunity

In LTGG, we aim to balance imagination with discipline. Opportunities often emerge where the stockmarket underestimates tipping points or misjudges where margins accrue. The companies that capitalise on these opportunities rarely conform to traditional analyst models. And as is typical for LTGG, the distribution of returns has been skewed.

Tesla is an excellent case in point. In the early days, many industry analysts dismissed its ability to reinvent automotive operating models, but we saw things differently. A 2013 LTGG research note captured the logic well: “Tesla’s value lies not in what in can do between now and 2015, but in what it can do over the next decade and more. What do you pay for a company with disruptive potential in a global industry worth trillions of dollars?”

Tesla broke the mould across almost every aspect of its business and supply chain and was often misunderstood by traditional auto sector analysts. The journey to outlier returns was an extremely bumpy one as a result, with four drawdowns of over 50 per cent along the way, and another eight drawdowns in excess of 30 per cent. Holding on through the numerous drawdowns to unlock a 79x return over our 12-year holding required intestinal fortitude and a patient client base.

Our experience of navigating transformations in energy and mobility has reinforced the need to look beyond the narrow confines of the finance industry.

Over the years, our stock picking insights have been enriched by external thinkers such as Doyne Farmer (American author, scientist and entrepreneur) and Jessika Trancik (MIT professor), and partnerships with institutions including Tsinghua, Sussex and the Whittle Laboratory. Our unparalleled access to private companies has further sharpened our ability to calibrate the probabilities and possibilities ahead.

The opportunities looking forward

Three-quarters of the world's population lives in net fossil-importing nations. Only North America is largely energy self-sufficient. Over the next decade, a quest for energy security will accelerate the energy transition.

Global electricity consumption has doubled since LTGG began. Rising incomes, heat-stress adaptation, mobility electrification and the energy needs of distributed AI point towards further sharp increases in the years ahead.

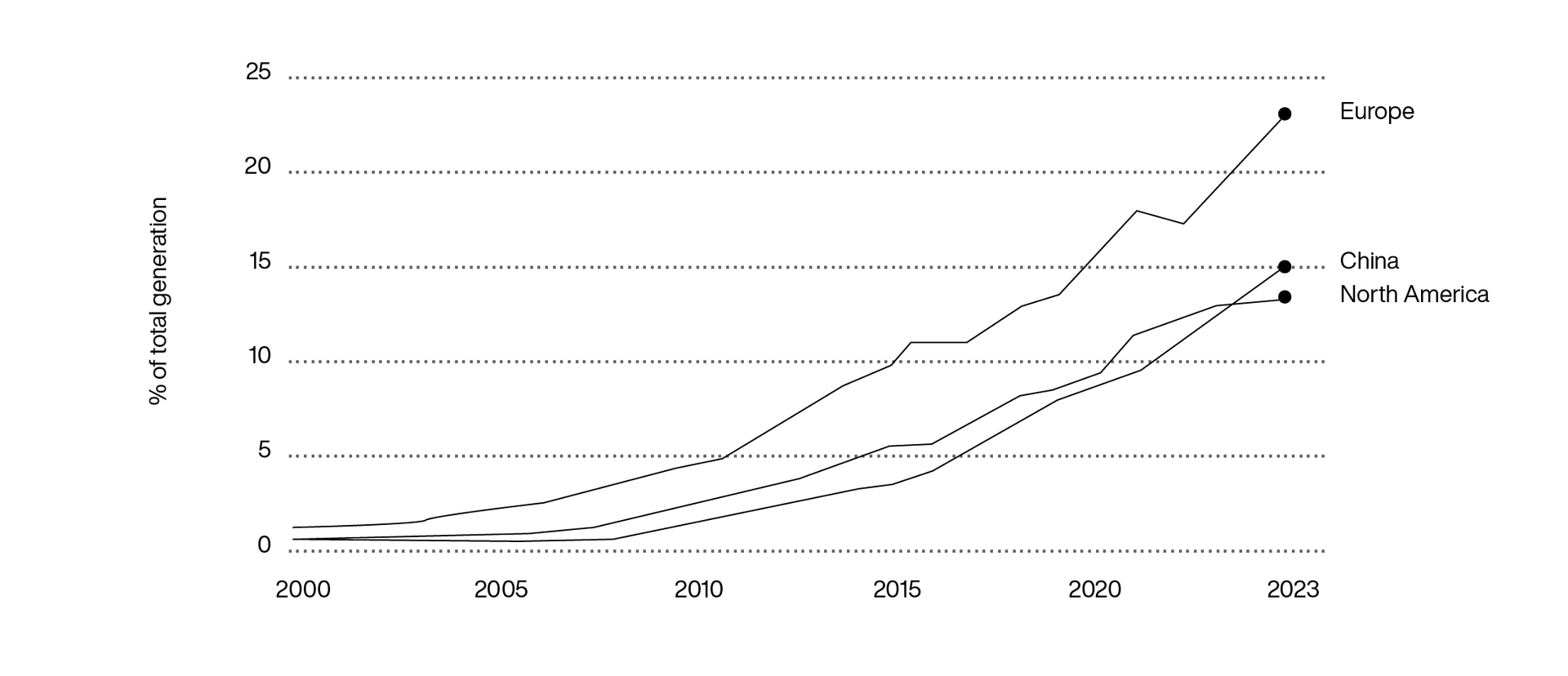

Renewables still account for less than a quarter of electricity generation in major economies, but trajectories point towards a share of roughly half within the next two decades.

China already operates the world’s largest electric power industry and is on course to become the first true ‘electro state’, supported by greater policy stability and fewer shifting goalposts. However, in our view, there is scant likelihood of making money from direct renewable investments. Returns are unexciting, products are commoditised, and there are frequent overcapacity issues.

Solar and wind generation

The next energy lynchpin

LTGG has found a far more interesting opportunity in Contemporary Amperex Technology Limited (CATL).

Its visionary yet discreet founder, Robin Zheng – the ‘invisible king’ – has transformed Ningde into a global battery powerhouse.

CATL now enjoys a clear technology lead and is the employer of choice for many of the brightest STEM graduates. Profits have surged over the last five years, and there’s plenty more to come.

We’ve known Robin since 2017 when CATL was still private, and our conviction has been strengthened by our deep networks with other key players in the battery ecosystem.

More recently, CATL has been quietly morphing into an integrated energy-solutions provider. Its rapidly growing Energy Storage Systems business deploys large battery systems to store electricity for industrial, commercial and residential applications. The battery recycling business is ramping fast, and CATL’s world-leading research and development continues to deliver breakthroughs, including an EV battery with 1500km of range and another that can charge fully in six minutes. CATL’s valuation seems perplexingly meagre compared to the oil majors. A decade from now, we suspect that many will reflect on this with bemusement.

Future operating systems

The rise of China's auto industry has been remarkable. But, as with renewables, significant overcapacity suggests consolidation is likely. As with energy infrastructure, we need to carefully assess where the value will accrue.

We believe the most compelling opportunities may lie within China's autonomous driving ecosystem, supported by high urban vehicle density and a deep pool of software engineering talent.

In this context, our holding in Horizon Robotics stands out. An emerging leader in autonomous-driving computing, it has long been on our radar. We’ve known the founder since well before the company went public, giving us rare insight into its distinctive culture. Horizon Robotics has deepening partnerships with over twenty of the largest domestic EV companies and looks uniquely well placed to earn handsome royalties as domestic auto mileage scales.

Reaching for the sky

Our exploration of electric mobility now extends into aviation. In Joby Aviation, we see an opportunity shaped by the market's reluctance to embrace uncertainty in a nascent but potentially vast industry.

Joby’s early eVTOL work began in a barn. Today, founder JoeBen Bevirt leads more than 1,500 colleagues who describe him as both visionary and detail-obsessed. Baillie Gifford invested privately in 2019, with LTGG initiating a position after the public listing in 2023.

Progress has been significant: the final stages of FAA certification are being cleared; successful test flights completed; pre-commercial operations launched; partnerships with Toyota and the US Department of Defence strengthened; and a new manufacturing facility established to enable scale.

JoeBen’s long-term mission is bold: to “eat Boeing from the inside out”. And we believe that there’s a small but growing possibility of that mission being accomplished.

The breadth of the evolving opportunity across energy and mobility is striking.

These examples highlight the importance of remaining open-minded, imaginative and curious. The answers rarely sit in the spreadsheets of traditional analysts. And therein lies our opportunity.

Exploring different questions

We continue to explore questions that receive less attention than they should from market participants:

Do car brands matter in a world of autonomy or is the auto proposition one of a fleet operator?

How likely is solid state and what bearing does this have on the battery proposition?

How do geopolitics affect raw materials supply and addressable markets?

How does the insurance industry evolve in a world of autonomy?

Is the future of hydrogen based around energy storage or an energy source?

What is the role of nuclear power in addressing energy consumptive AI?

Is the future of the energy grid entirely decentralised?

How rapidly will emissions pricing evolve – in both cost and scope?

What are the second order implications of autonomy on tyres, insurance, confectionary and streamed entertainment?

Disclaimers

Annual performance to 31 March each year (net %)

| Investment type | 2022 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|

| Baillie Gifford Long Term Global Growth Investment Fund B-ACC | -10.3 | -16.7 | 26.9 | 5.9 | -2.3 |

| MSCI ACWI Index* | 12.8 | -0.9 | 21.1 | 5.3 | 18.0 |

| IA Global Sector | 8.4 | -2.7 | 16.7 | -0.3 | 13.4 |

Past performance is not a guide to future returns

The Long Term Global Growth Investment Fund aims to outperform (after deduction of costs) the MSCI ACWI Index, as stated in sterling, over rolling five-year periods. Prior to 1st July 2023, to outperform (after deduction of costs) the FTSE All-World index, as stated in Sterling, over rolling five-year periods. The manager believes this is an appropriate target given the investment policy of the Fund and the approach taken by the manager when investing. In addition, the manager believes an appropriate performance comparison for this Fund is the Investment Association Global Sector.

There is no guarantee that this objective will be achieved over any time period and actual investment returns may differ from this objective, particularly over shorter time periods.

Important Information

This communication was produced and approved in May 2026 and has not been updated subsequently. It represents views held at the time of writing and may not reflect current thinking.

This communication does not constitute, and is not subject to the protections afforded to, independent research. Baillie Gifford and its staff may have dealt in the investments concerned. The views expressed are not statements of fact and should not be considered as advice or a recommendation to buy, sell or hold a particular investment.

Baillie Gifford & Co Limited is authorised and regulated by the Financial Conduct Authority. Baillie Gifford & Co Limited is an Authorised Corporate Director of OEICs.

A Key Information Document is available at bailliegifford.com.

Investment markets can go down as well as up and market conditions can change rapidly. The value of an investment in the Fund, and any income from it, can fall as well as rise and investors may not get back the amount invested.

The specific risks associated with the Fund include:

- Custody of assets, particularly in emerging markets, involves a risk of loss if a custodian becomes insolvent or breaches duties of care.

- The Fund invests in emerging markets, which includes China, where difficulties with market volatility, political and economic instability including the risk of market shutdown, trading, liquidity, settlement, corporate governance, regulation, legislation and taxation could arise, resulting in a negative impact on the value of your investment.

- The Fund's concentrated portfolio relative to similar funds may result in large movements in the share price in the short term.

- The Fund has exposure to foreign currencies and changes in the rates of exchange will cause the value of any investment, and income from it, to fall as well as rise and you may not get back the amount invested.

- The Fund's share price can be volatile due to movements in the prices of the underlying holdings and the basis on which the Fund is priced.

Further details of the risks associated with investing in the Fund can be found in the Key Investor Information Document or the Prospectus, copies of which are available at bailliegifford.com.